Travel Hacking for Beginners: How to Fly for Free with Points in 2026

Learn how to earn 267,000+ points in your first year and book business class flights for free. A complete beginner's guide to travel hacking in 2026.

Learn how to earn 267,000+ points in your first year and book business class flights for free. A complete beginner's guide to travel hacking in 2026.

Travel hacking sounds like it requires a hoodie, a dark room, and questionable morals. It doesn't.

It's the art of earning credit card points and airline miles strategically — then redeeming them for flights and hotels that would otherwise cost thousands. No fraud. No loopholes. Just smart optimization.

And in 2026, signup bonuses are at historic highs. We're talking 75,000 to 175,000 points on a single card — enough for a round-trip business class ticket to Tokyo from one welcome offer.

Travel hacking is earning points and miles through credit card signup bonuses, everyday spending, shopping portals, and dining programs — then redeeming them for flights and hotels at a fraction of cash prices.

The key insight: a point worth 1 cent as cash back can be worth 4 to 8 cents when redeemed for a premium cabin through the right airline partner. You're not breaking rules. You're just playing the game better than most people realize is possible.

A typical beginner can accumulate 150,000 to 200,000 transferable points in their first year through signup bonuses and category spending alone. No manufactured spending required.

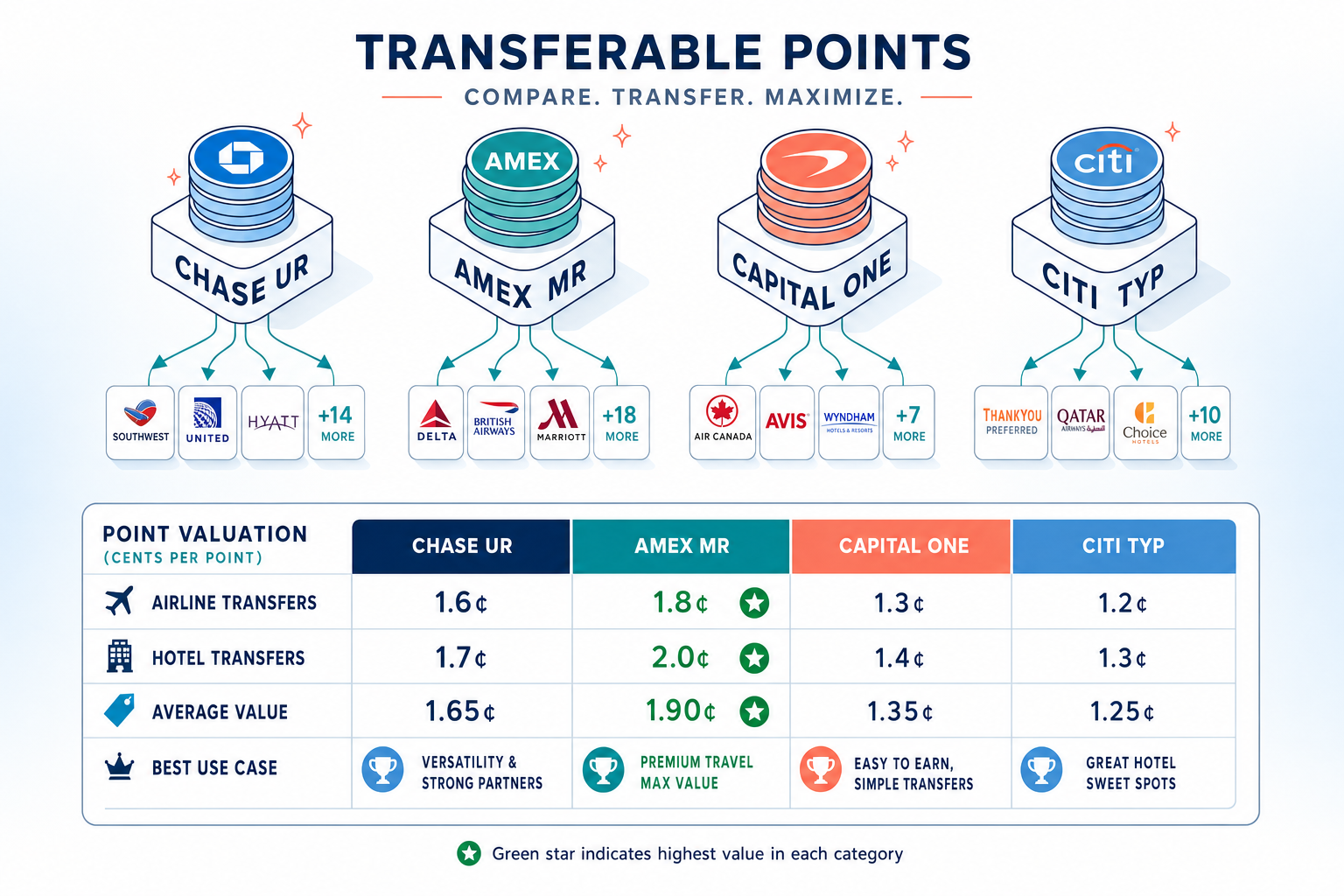

There are two types of rewards currencies, and understanding the difference is the single most important concept in travel hacking.

Fixed-value points are worth a set amount — usually 1 cent — no matter how you redeem them. Simple, but limited upside.

Transferable points are the crown jewels. They move to airline and hotel partners at a 1:1 ratio, where their value multiplies dramatically. The four major transferable currencies are your entire toolkit.

When you use a tool like Autopilot to search for flights, you can see exactly where your points will stretch furthest — which makes picking the right transfer partner effortless.

These are the building blocks of every travel hacker's strategy. Each one transfers to different airline and hotel partners, meaning the "best" currency depends on where you want to go.

| Currency | Best Earn Rate | Top Transfer Partners | Average Point Value | Best For |

|---|---|---|---|---|

| Chase Ultimate Rewards | 3x dining, 5x Chase Travel | Hyatt, United, Southwest, Air Canada | 2.0 cents | Hotels (Hyatt), domestic flights |

| Amex Membership Rewards | 4x dining & groceries, 5x flights | ANA, Virgin Atlantic, Air France, Delta | 2.0 cents | Premium international cabins |

| Capital One Miles | 2x everything, 10x hotels/cars | Air Canada, Turkish Airlines, TAP Air Portugal | 1.7 cents | Flat earn rate, Turkish sweet spots |

| Citi ThankYou Points | 3x dining, hotels, flights, groceries | Turkish Airlines, Virgin Atlantic, Air France | 1.7 cents | Turkish domestic sweet spot |

Those "average point values" are conservative. On the right redemptions — ANA First Class, Hyatt peak-season hotels — you can hit 5 to 10 cents per point. That's where travel hacking gets genuinely absurd.

Your first card matters. Here's where to start, ranked by value-for-difficulty.

| Card | Signup Bonus | Minimum Spend | Annual Fee | Why It's Great for Beginners |

|---|---|---|---|---|

| Chase Sapphire Preferred | 75,000 points | $5,000 / 3 months | $95 | Best all-around starter card. Transfers to Hyatt, United, Southwest. |

| Capital One Venture X | 75,000 miles | $4,000 / 3 months | $395 (offset by $300 travel credit + 10K anniversary miles) | Effectively $95/year net cost. Lounge access included. |

| Citi Strata Premier | 70,000 points | $4,000 / 3 months | $95 | Underrated. Turkish Airlines transfer = 10K miles for domestic flights. |

| Amex Gold | Up to 100,000 points | $8,000 / 6 months | $325 | 4x on dining and groceries. Best everyday earn rate. |

| Chase Sapphire Reserve | 150,000 points | $6,000 / 3 months | $795 (offset by $300 travel credit) | Massive bonus for higher spenders. Priority Pass lounge access. |

The play for most beginners: Start with the Chase Sapphire Preferred. The $95 fee is trivial compared to the 75,000-point bonus (worth $1,500+ through transfer partners), and it gets you into the Chase ecosystem before the 5/24 rule becomes relevant.

Signup bonuses are where 80% of your points come from in year one. The strategy is straightforward.

Step 1: Apply for one card at a time. Meet the minimum spend through your normal everyday purchases — groceries, gas, subscriptions, bills. No manufactured spending needed.

Step 2: Once you've earned the bonus, wait 90 days and apply for the next card. This gives your credit score time to recover from the hard inquiry (more on that below).

Step 3: Keep all cards open for at least 12 months before considering a downgrade or cancellation. Annual-fee cards can often be downgraded to no-fee versions to preserve your credit history.

| Month | Action | Points Earned | Running Total |

|---|---|---|---|

| Month 1 | Open Chase Sapphire Preferred, start meeting $5,000 spend | — | — |

| Month 3 | Hit spending requirement, earn 75,000 Chase UR bonus | 80,000 | 80,000 |

| Month 4 | Apply for Capital One Venture X or Citi Strata Premier | — | 80,000 |

| Month 6 | Hit second bonus (70,000–75,000 points) | 77,000 | 157,000 |

| Month 7 | Apply for Amex Gold (if spending supports $8K in 6 months) | — | 157,000 |

| Month 12 | Hit Amex Gold bonus + everyday earning all year | 110,000 | 267,000 |

267,000 points in year one. That's enough for two round-trip business class tickets to Europe, or four to five domestic round-trips, or a week at a luxury Hyatt resort. All from spending money you were going to spend anyway.

Most travel hackers earn the majority of their points on the ground. Here's how.

The Amex Gold earns 4x on dining and groceries. If your household spends $1,500 a month in those categories, that's 72,000 points per year — before the signup bonus. Stack that with the Chase Sapphire Preferred's 3x on dining for any spending the Amex doesn't cover.

Rakuten, the airline shopping portals, and Chase Offers all pay bonus points on purchases you're making anyway. The trick: you can stack portal earnings with your credit card rewards. A purchase through Rakuten on an Amex card earns points from both sources simultaneously.

Programs like Seats at the Table (Amex) and Chase Dining Rewards let you earn bonus points at participating restaurants — on top of your card's regular dining multiplier.

This is where it all pays off. These are the redemptions that deliver genuinely outsized value.

| Redemption | Points Required (One-Way) | Cash Price | Value Per Point | How to Book |

|---|---|---|---|---|

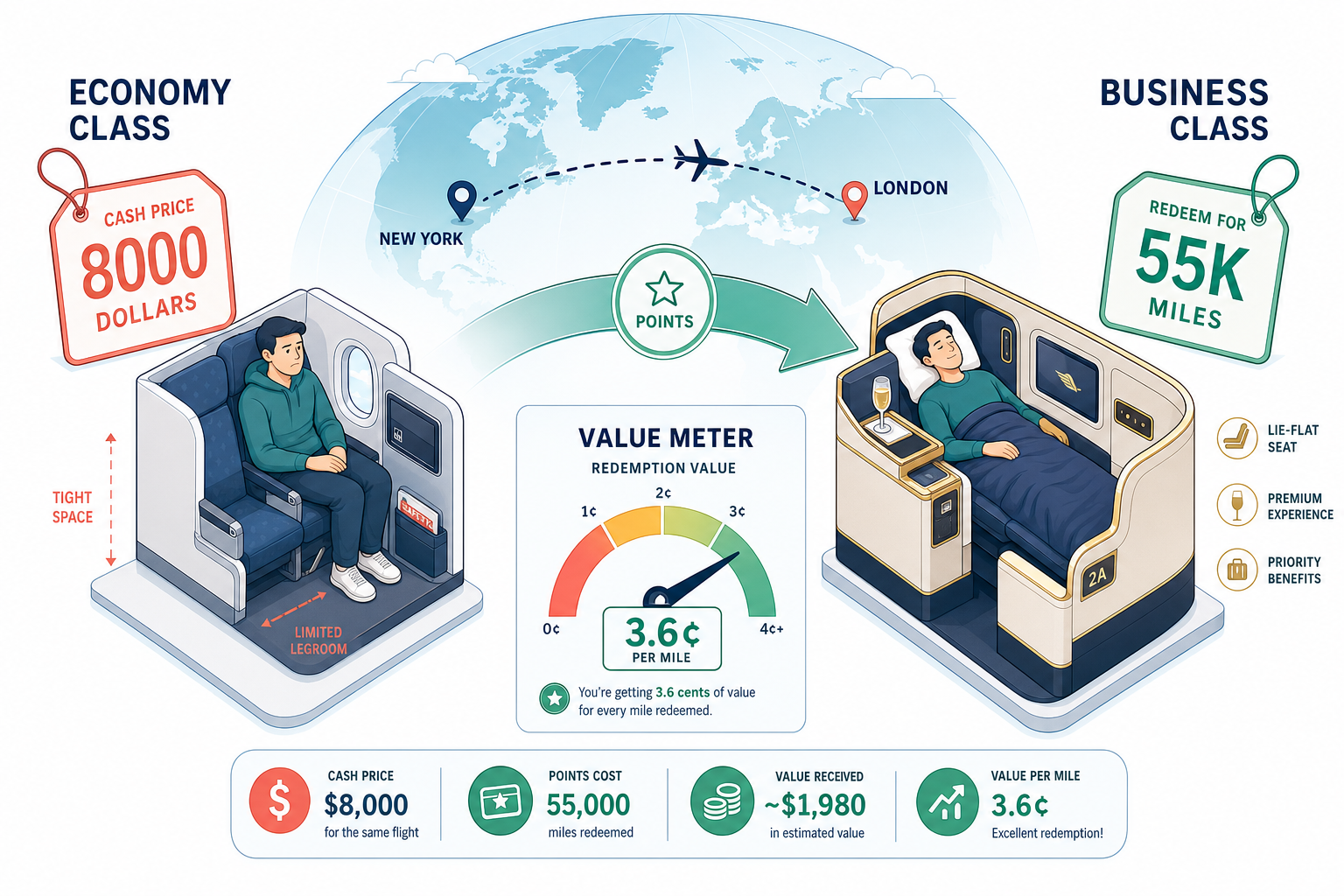

| ANA First Class (The Suite) to Tokyo | 55,000–60,000 Virgin Atlantic miles | $10,000+ | ~17 cents | Transfer Chase/Amex/Citi to Virgin Atlantic |

| Hyatt Category 1–4 Hotels | 3,500–15,000 per night | $150–$500 | 3–5 cents | Transfer Chase UR to World of Hyatt |

| Turkish Airlines Domestic US Flights | 10,000 miles one-way | $200–$400 | 2–4 cents | Transfer Citi/Capital One to Turkish Miles & Smiles |

| Air France Flying Blue Promo Awards | 18,000–30,000 miles to Europe | $600–$1,200 | 3–4 cents | Transfer Chase/Amex to Flying Blue (monthly promos) |

| Alaska Short-Haul Economy | 4,500 Atmos Rewards one-way | $100–$200 | 2–4 cents | Book directly through Alaska (under 700 miles) |

The ANA First Class redemption is the single best sweet spot in the hobby. A $10,000+ seat for 55,000 miles transferred from a Chase or Amex card. If that doesn't convince you travel hacking is worth learning, nothing will.

Planning a trip and want to see exactly where your points go furthest? Autopilot shows you real-time award availability across airlines — so you never leave value on the table.

Avoid these and you'll be ahead of 90% of people who try travel hacking.

Carrying a balance. This is the cardinal sin. Even one month of interest charges can wipe out the value of your entire signup bonus. If you can't pay the statement in full every month, travel hacking is not for you yet. Get your finances in order first.

Ignoring the Chase 5/24 rule. Chase will deny your application if you've opened five or more credit cards (from any issuer) in the past 24 months. Since Chase has the best beginner cards, always start there before branching out to Amex or Capital One.

Redeeming at 1 cent per point. Using Chase points for cash back or statement credits gives you 1 cent per point. Transferring to Hyatt can get you 4 to 5 cents. Transferring to Virgin Atlantic for ANA First can get you 17 cents. Never take the lazy redemption.

Opening too many cards too fast. Spacing applications 90 days apart gives your score time to recover and improves your approval odds. Patience pays — literally.

Forgetting to meet minimum spend. You get exactly zero bonus points if you fall short by even a dollar. Track your spending carefully in the first three months.

This is the most common concern — and it's mostly a myth.

Each credit card application triggers a hard inquiry that temporarily drops your score by 5 to 10 points. That recovers within 90 days. Meanwhile, the new card increases your total available credit, which lowers your utilization ratio — one of the biggest factors in your score.

The data backs this up: most experienced travel hackers hold 10 to 20+ cards and maintain credit scores of 750 to 800+. The key is paying every statement in full and on time, keeping utilization low, and never closing your oldest cards.

One real caveat: If you're planning to apply for a mortgage or major loan in the next 6 to 12 months, hold off on new card applications. The temporary score dips, while small, can affect your rate at the worst possible time.

The points and miles world moves fast. Here's what's different this year.

Signup bonuses are at historic highs. The Chase Sapphire Reserve is offering 150,000 points — that was unthinkable two years ago. Amex Gold is running targeted offers up to 100,000 points. If you've been waiting to start, 2026 is arguably the best entry point ever.

Devaluations are accelerating. Aeroplan overhauled its award chart effective June 1, 2026, raising prices on 85% of routes. Cathay Pacific Asia Miles and Avianca LifeMiles both devalued earlier this year. The trend is clear: points are worth less every year, so earn and burn — don't hoard.

Dynamic pricing is expanding. More airlines are moving away from fixed award charts toward revenue-based pricing for award seats. This makes transfer partner sweet spots (like ANA via Virgin Atlantic) even more valuable — they're the last holdouts of outsized value.

The Chase 5/24 rule still stands. Despite rumors, Chase hasn't loosened its stance. However, they now allow holding both Sapphire cards simultaneously, which is a new development for 2026.

All the more reason to start now rather than later. And if you want to stay on top of award availability and price drops, Autopilot monitors flights for you so you can book the best deals the moment they appear.

Yes, completely. You're signing up for credit cards, meeting spending requirements with legitimate purchases, and redeeming points through the programs' own channels. There's nothing illegal or gray-area about it.

You don't need extra money — you redirect existing spending to the right cards. If your household spends $1,500 to $2,000 per month on everyday expenses, that's enough to meet most signup bonus requirements within 3 months. Never spend more than you normally would just to earn points.

Most premium travel cards require a score of 670+, with best approval odds above 720. If your score is lower, start with a no-annual-fee card like the Chase Freedom Unlimited to build history. You can upgrade once your score improves — typically within 6 to 12 months.

There's no magic number. Many experienced travel hackers hold 15 to 25 cards with excellent scores. The key is paying every card in full and only opening cards whose bonuses justify the effort. For beginners, 2 to 3 new cards in the first year is a comfortable pace.

Airline miles (like Delta SkyMiles) can only be used with that specific airline. Transferable points (like Chase Ultimate Rewards) can move to multiple airlines and hotels, giving you far more flexibility and usually better value per point.

Not at all. Most travel hackers earn the majority of their points through credit card spending, signup bonuses, and shopping portals — all on the ground. Many people accumulate hundreds of thousands of points without ever setting foot on a plane.

Chase UR and Amex MR points never expire as long as your account is open. Capital One miles don't expire while your account is in good standing. Citi ThankYou Points expire after 12 months of inactivity. Once transferred to airline or hotel programs, each has its own policy — typically 18 to 24 months of inactivity.

Use them. With airlines and hotels consistently devaluing their award charts — Aeroplan, Cathay Pacific, and Avianca LifeMiles all raised prices in 2026 alone — points are almost always worth less tomorrow than they are today. Earn a bonus, find a great redemption, and book it. Hoarding points is the most common (and most expensive) beginner mistake.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Credit card offers, signup bonuses, and program terms are subject to change. Always read the full terms and conditions before applying for any credit card. Travel hacking involves responsible credit management — never spend beyond your means to earn points. Autopilot is a travel technology platform and is not affiliated with any credit card issuer or loyalty program mentioned in this article.